Select Retail Sales Increased in 2020

Autosphere » Mechanical »

the picture that emerges of the aftermarket in 2020 is mixed but shows real strength relative to the rest of the automotive sector, the automotive aftermarket was not affected as deeply as the new vehicle market or the manufacturing side of the industry. PHOTO Huw Evans

Throughout 2020, the impacts of the pandemic on the automotive industry were evident in key areas. New light vehicle sales saw record-setting decreases, finishing the year down 19.7%.

Production from the high profile assembly sector decreased sharply, falling 26.9% for the year as the supply chain shut down. However, the picture for the automotive aftermarket in Canada was nowhere near as dire.

“Many assumptions made by generalist consulting companies and economists with limited understanding of the aftermarket proved to be overly negative” commented DAC “The aftermarket has long been the backbone of the Canadian auto industry and continued to hold strong throughout the pandemic, at least compared to other industry sub-sectors.”

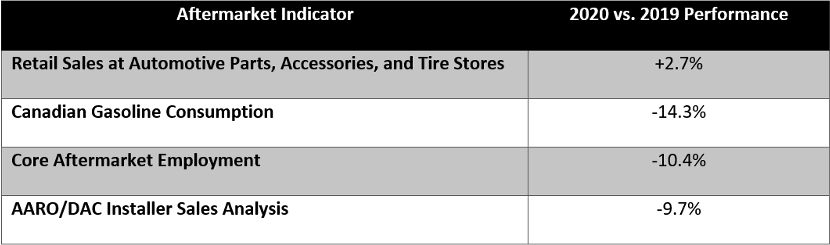

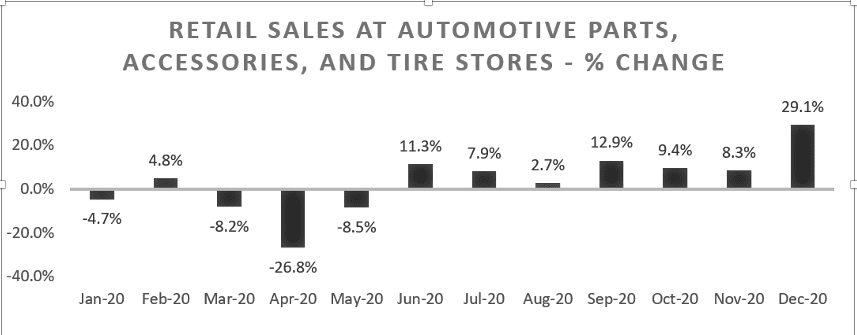

Indeed, analysis by DAC of recently released Statistics Canada data shows that retail sales at automotive parts, accessories, and tire stores surprisingly increased 2.7% in 2020 from 2019 levels.

While sales at these outlets did indeed fall in the Spring during the first wave of the pandemic, the drop in March, April, and May was relatively subdued and retail sales figures bounced back quickly.

The Fall was particularly strong, leading to overall retail sales at automotive parts, accessories, and tire stores to increase to $10.62 billion in 2020.

Now, parts and tire stores are by no means the aftermarket as a whole, and at DAC we always like to look deeply at a wide array of variables when judging the health of a sector.

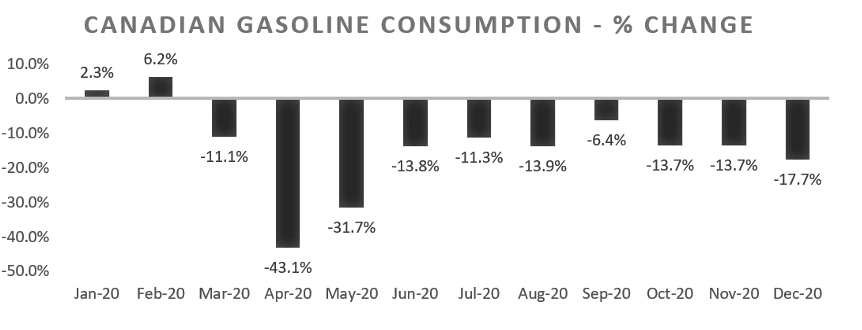

Gasoline consumption can be a useful indicator of kilometres driven and how much Canadians are using their vehicles. At the height of the first wave of pandemic-related restrictions, gasoline consumption dropped 43.1% for the month of April.

While gasoline consumption did not remain as low, it still remained well below 2019 levels through to the end of the year. Overall, gas consumption dropped 14.3% in 2020, a fall that would undoubtedly lead to decreases in some (but not all) vehicle maintenance categories.

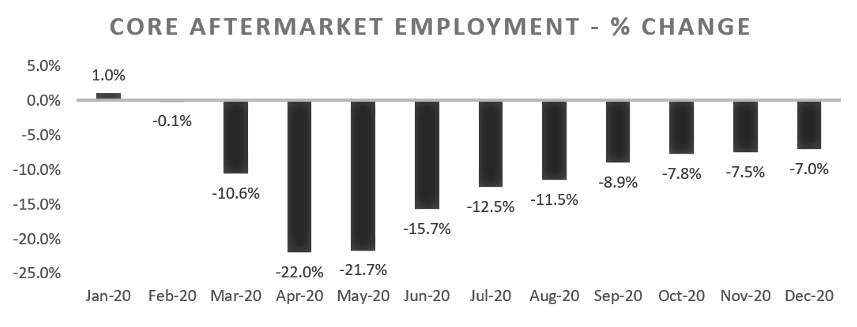

Employment figures for the core aftermarket industries—comprised of motor vehicle parts and accessories wholesale, automotive parts and accessories stores, and automotive repair and maintenance—were down in 2020, by an average of 10.4%.

However, the sharp decline in the Spring gave way to a steady partial recovery, with total employment counts as of December 2020 down 7.0% from 2019.

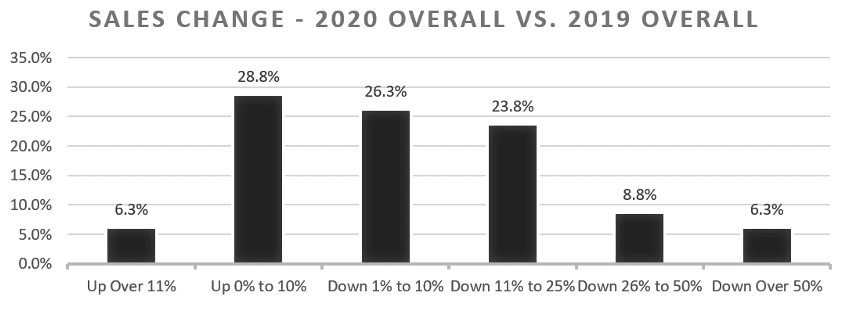

In terms of direct feedback from aftermarket installers, DAC conducted a survey in late January with our colleagues at Automotive Aftermarket Retailers of Ontario (AARO) in order to better understand the impacts of the pandemic on independent installers.

AARO members indicated mixed performance in 2020 with the largest group of respondents (28.8%) indicating sales increases of 0-10%, while the next largest group (26.3%) indicated small decreases of less than 10%.

In summary, the picture that emerges of the aftermarket in 2020 is mixed but shows real strength relative to the rest of the automotive sector. The automotive aftermarket was not affected as deeply as the new vehicle market or the manufacturing side of the industry.

While the aftermarket was still negatively impacted by the pandemic, the mixed performance and relatively strong retail sales figures indicated a measure of deep-rooted stability. Hopefully this stability remains in 2021 as Canada navigates the current third wave of the pandemic and the industry faces yet further challenges.

JOBS

|  VAL-DAVID VAL-DAVID Full time Full time |

| NAPIERVILLE Full time |

| SAINT-BASILE-LE-GRAND Full time |

| SAINT-BASILE-LE-GRAND Full time |

| MONTRÉAL Permanent |