Subscribe to our Autosphere magazine and our weekly newsletter to get the latest industry news.

Automotive News, Expert Advice, and How-tos

Market for EV Powertrain Materials to Reach $47 bn by 2030

Autosphere » Mechanical »

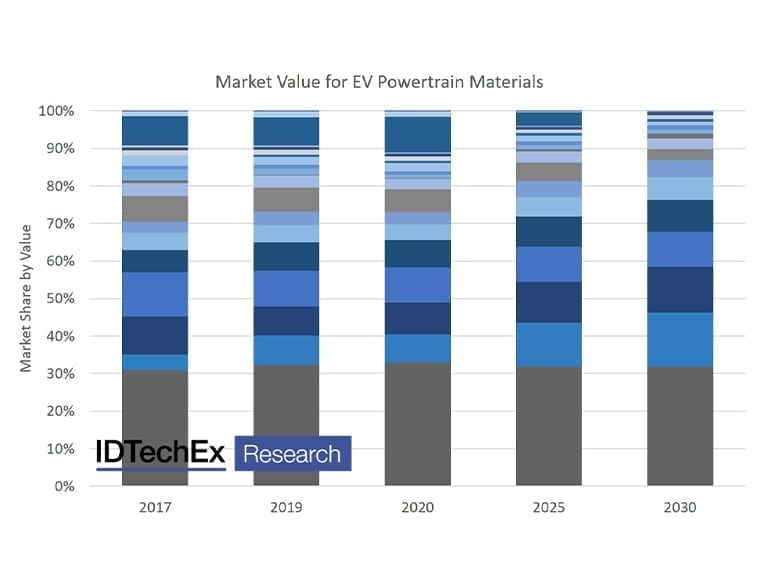

IDTechEx forecasts over 28 materials used in the construction of electric vehicle powertrains, each with shifting market shares. A rapid increase in demand is seen across several material markets after a small drop in 2020 due to COVID-19 implications for the automotive market. Source: IDTechEx Research, “Materials for Electric Vehicles 2020-2030”.

Traction batteries and motors in electric vehicles (EVs) are very different to the powertrain components of the internal-combustion engine vehicles they replace. There will be a much greater demand for several materials markets which otherwise would see only modest growth.

For example, while the combustion engine and transmission relies heavily on aluminum and steel alloys, Li-ion batteries alone also require a great deal of nickel, cobalt, aluminum, lithium, copper, insulation, thermal interface materials and much more at the cell and pack level.

The new report from IDTechEx, “Materials for Electric Vehicles 2020-2030”, identifies and analyses trends in electric vehicle battery cell- and pack-level materials, and electric traction motor materials, to determine the overall materials demand from the construction and future improvements of these components. For each, a granular breakdown is used to forecast each material required and its market value over the next 10 years.

Battery Cell Materials

Several of the raw materials used in electric vehicle components have questionable mining practices or volatile supply chains, leading OEMs to change the way they make batteries and motors. A commonly used cathode material, cobalt, has questionable mining practices. It’s also a very expensive material with its supply and mining confined to a large majority in China and the Democratic Republic of Congo. As a result, OEMs are trending towards the use of higher nickel cathode chemistries such as NMC 622 and even NMC 811 in some new vehicles.

Another significant trend is the phase-out of LFP cathodes. The Chinese electric car market was, up until 2018, predominantly using LFP cathodes. This has now transitioned so that in 2019 only 3% of new cars were using LFP, however, the introduction of the Tesla Model 3 in China using LFP could upset this trend. Despite the reduction in the market share of materials like cobalt, the rapidly increasing market for electric vehicles will drive demand for cobalt and many other materials drastically higher over the next 10 years.

Battery Pack Materials

Cell energy density is increasing, but pack energy density is increasing. With manufacturers improving battery designs, the mass of materials being used around the cells is steadily being reduced allowing for a lighter battery pack or more cells to be used for the same mass. This is largely affected by the choice of material for the enclosure—OEMs are more interested in composite utilization. The thermal management strategy also has a significant impact. This includes the choice of active or passive cooling variants, thermal interface materials, thermal runaway prevention and fire-retardant materials. With greater energy density and consumer demand for fast charging, more effective thermal management is required in a smaller and lighter package. This may lead to a decrease in many battery pack materials per vehicle, but this is likely to be overshadowed by the total market increase for EVs.

Electric Motor Materials

Along with batteries, the demand for electric traction motors will increase rapidly over the next 10 years, not just from the overall vehicle sales but also with the rise of vehicles using more than one motor, specifically in premium cars and heavy-duty vehicles. Critical to materials, the majority of the EV market is using motors with permanent magnet-based rotors. These materials typically contain several rare-earths such as neodymium and dysprosium, both of which have a very geographically constrained supply chain and a volatile price history. Whilst they are in a relatively small quantity in the motor, they can make up a very significant portion of the cost of the motor. We are seeing some manufacturers like Renault using motors with no magnets, whereas Tesla has transitioned to a magnet-based motor for the potential improvements in efficiency which can increase range thus reducing the requirements for other critical battery materials.

Another key question is recyclability. Often overlooked at the development stage, when a motor/vehicle reaches end of life, is it easy to remove the expensive, critical materials used in the magnets or windings? Most current designs don’t take this into account and whilst we’re seeing some manufacturers switching to motors with less expensive or easier to recycle raw materials, the vast majority are focussing on incremental improvements to the efficiency of current designs.

Tags : Sales and Marketing

JOBS

|  SAINT-EUSTACHE SAINT-EUSTACHE Full time Full time |

| SALABERRY-DE-VALLEYFIELD Full time |

| BOUCHERVILLE Full time |

| MONTRÉAL-NORD Full time |

| MONTRÉAL Full time |