Electric Buses Growing Towards a 50 Percent Global Market Share

Autosphere » Fleet »

Arthur D. Little published a study on use and future use of completely electrical buses. Photo: Arthur D. Little

Global management consultancy, Arthur D. Little, has published a new report on electric buses.

Electric buses are expected to be more efficient and greener than diesel buses, and key to making cities more environmentally friendly.

Every city must carefully choose its individual solution for its bus fleet, and OEMs have to be ready to mirror the local requirements by understanding the needs of both PTOs and PTAs.

According to the United Nations forecast, the global level of urbanization will grow from 55% in 2018 to 68% by 2050, adding 2.5 billion people. This will place an extra burden on already significantly overloaded transportation systems – in most traffic-congested cities, such as Mexico City, Moscow, Paris, Rome and London, drivers spend more than 200 hours in congestion per year already. This has forced cities to start using road infrastructure much more effectively and increase their shares of public transport, among other measures.

At the same time, ongoing development of transportation systems constitutes a major ecological challenge – road transport accounted for almost 20% of total CO2 emissions in 2016. Although the amount of CO2 emissions per passenger for an average diesel bus is slightly lower than for an internal combustion engine (ICE) car, the shift to public transport alone is certainly not enough to address this problem. As a result, the challenge to make public transport environmentally friendly is becoming one of the most important priorities for cities.

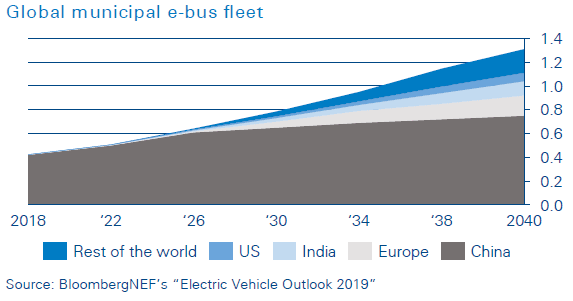

The shift to ecological urban road public transport has already begun – diesel buses are being banned in cities around the world, and fully electric, plug-in hybrid, natural gas (CNG), and fuel cell buses that reduce urban noise and do not pollute are increasing. The leader of this transformation is China, where 99% of the global electric bus fleet was located at the end of 2018 (421,000 out of 425,000 electric buses, according to a Bloomberg NEF report released in May 2019), and the share of electric buses is about 18% of the total municipal bus fleet. According to the IEA Global EV Outlook 2019, the number of electric buses in 2018 was even higher, approximately 460,000 electric buses globally. In major cities such as Shenzhen, all ICE buses have been replaced with e-buses, helped by a supporting policy from the government and PTAs. However, the annual growth rate of the e-bus fleet will slow down due to termination of subsidies, which will take effect by the end of 2020.

For every 1,000 electric buses, demand for diesel can be decreased by up to 500 barrels per day. Although there were only about 3,000 electric buses in Europe and the US in 2019 (approximately 1% of buses on the roads in these regions), this number will grow rapidly in the coming years. China has had subsidies for the last decade, and now many other countries, such as Russia, Sweden and India, also offer these to support the growth of electric buses. Simultaneously, a number of other large cities, including London and Los Angeles, have committed to procuring only zero-emission buses starting in 2025. By 2040, electric buses could exceed 1.3 million globally and form more than 50% of the total bus fleet (see figure below).

Case examples:

India has a government plan for 10,000 electric buses initially.

Chile plans to increase its number of electric buses from approximately 400 in 2019 to 2,000 in 2022. In addition, Chile has a national target of 100% electric public transportation by 2050.

Moscow intends to abandon purchasing of diesel buses after 2021 and procure 600–800 electric buses annually.

Paris plans to buy more than 800 electric buses in the coming years.

Colombia will total more than 550 electric buses, with a recent contract awarded to BYD for 379 electric buses in Bogota.

In Sweden in November 2019, Volvo announced a record order of 157 electric buses from Transdev to serve Gothenburg.

The US has a goal of making 33% of all transit buses electric by 2045.

However, despite the great prospects for electric buses, their current usage is complicated by a number of challenges.

Current challenges for participants in the electric bus ecosystem

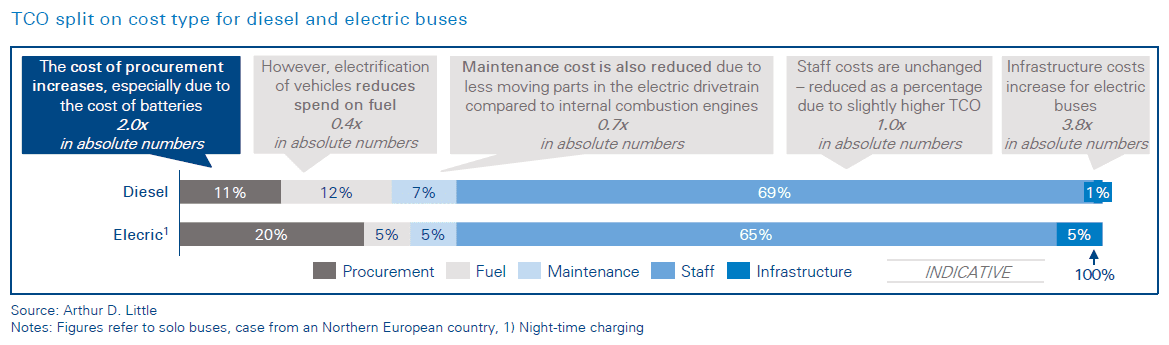

High up-front cost despite comparable TCO. Despite the fuel economy and cheaper maintenance of electric buses, their purchase implies significant up-front costs for operators – the cost of an electric bus with charging infrastructure is twice or three times that of a diesel bus (see figure below). The comparison is distorted by subsidies, notably to BYD in China.

Technical difficulties with operation. Currently, electric bus technologies are not mature and bus operators do not have enough competencies for their operation. This leads to regular delays and breakdowns on routes, especially in the first years of operation. In cold or hot weather, an e-bus’s climate system can exceed 50% of its total energy consumption, which leads to significant range reduction.

Low margins and high risks for OEMs. Despite the high cost in comparison with that of diesel buses, e-bus production is significantly less profitable for OEMs, partly because of their small production volume. Another challenge is to ensure availability of the small electric bus fleet because operators usually require long-term service guarantees from electric bus manufacturers. It requires an additional cost to be integrated into bus operators’ business models and implies high risks due to insufficient operating experience and the uncertain residual cost of batteries. For example, unexpected battery failure could result in loss of approximately one-third of the electric bus’s cost.

Additional competition from new players. In addition to traditional OEMs, players from adjacent industries with strong competencies in electric motion have shown interest in the e-bus market. For example, Alstom, one of the largest manufacturers of railway transport, developed the electric bus Aptis, which was awarded the most innovative vehicle prize at Busworld, the well-known bus and coach exhibition event. Aptis has already received its first large order – 50 units for Paris operator RATP

Electric buses are not emission free and have other negative effects on the environment. Integration of electric buses into urban transport systems leads to additional emissions from electricity generation, which differ in significance depending on the types of power plants. On a global level, the environment is affected by toxic pollution generated by mining and refining of materials used in batteries; manufacturing of batteries themselves; and storing, treating or recycling of used batteries. (For more information, please see the viewpoint, “Battery electric vehicles vs. internal combustion engine vehicles”.)

TCO split on cost type for diesel and electric buses. Photo: Arthur D.Little

Outlook for further electric bus market development and key conclusions for market participants

Despite the current difficulties arising from the introduction of electric buses, the transition to environmentally friendly transport is inevitable. With improvements in technology, deepened competencies and more operational experience, electric buses will become a more economically viable solution compared to diesel buses. At the same time, the regions that are already introducing them provide an impetus for development of the industry in local areas – with not only production of electric buses, but also a number of related segments: charging stations, electrical components, batteries, etc. Players that are currently building up their competencies will claim leadership in the global fast-growing ecosystem.

To develop electric mobility successfully, cities, buyers and OEMs need to learn from others’ experience in operating electric buses and development in related industries. Based on our wide experience in electric mobility and advancement of urban systems, we highlight the following key points.

For cities and buyers of electric buses:

Evaluate the current energy and transport infrastructure for target electric bus solutions and adjust plans for development accordingly. For example, when using buses with overnight charging, a city may need to consider enhancing its power grids, so they can provide enough capacity to charge a large electric bus fleet at the depot. (For example, New York would have to open a new power plant to support its bus fleet going 100% electric.) Overnight charging also requires additional space because it is necessary to arrange a charger for each electric bus (compared with fueling stations, which only need to support a few buses concurrently), as well as power converters and power lines, in the depot.

Combine the fleet of electric buses with other ecologically friendly transport, making decisions separately for specific areas and routes and considering their features and availability of necessary infrastructure. For example, several cities in Switzerland (Lausanne, Bern and Geneva) are taking advantage of the well-developed trolleybus infrastructure, using trolleys with increased autonomous courses. This will allow them to build competencies in electric bus operations until the technology is fully mature.

Transitioning to electric buses may require a significant expansion of the fleet, especially when using electric buses with pantographs. These need to recharge at their end stations, and thus have shorter operation time. For example, Moscow’s trial electric bus routes have had to use almost twice as many buses as before to run the same services.

Start a dialogue with OEMs early. OEMs are interested in talking to both PTAs and PTOs to gain knowledge about the requirements that will come. By initiating early discussions and keeping OEMs updated, buyers will have a wider range of products to choose from.

Conclude agreements with OEMs under the conditions of a technical-readiness guarantee. This will reduce the risks associated with use of immature technology and allow development of the necessary competencies in electric mobility while working closely with OEMs.

In contracts with OEMs, cover responsibility for battery disposal. Ignoring this issue may lead to a conflict between the OEM and the city. For example, after a major contract had been signed and the electric buses had been delivered, it became clear that each of the parties involved had been confident that the other would be responsible for this.

For OEMs:

Provide a comprehensive solution, rather than a self-standing product, incorporating after-sales service and guarantees of technical readiness. The key is to develop an efficient logistics network for timely delivery of spare parts and integrate processes into the bus operator in the first years of operation. As the bus operator’s team deepens its competences and operations become well established, the after-sales model can be transformed from the constant presence of OEM employees “on site” to remote OEM support using Internet-of-Things and virtual-reality technologies.

Build alliances with players from related industries. For example, OEMs could partner with financial institutions to offer various financial instruments and reduce up-front costs for the customer. In addition to standard leasing tools, OEMs could offer diesel bus trade-ins and guarantees for buyback of electric buses at the end of the leasing term. This would relieve the operator of concerns about uncertain residual value. Another example involves alliances with charging infrastructure players, such as BYD’s collaboration with ENEL X in Chile and Colombia.

Lobby for incentives and favorable regulation, which are important factors in promoting the competitiveness of electric buses. For example, in Colombia electric bus programs started gaining momentum after the country passed a law in 2019 mandating that within six years all public transport service providers would have to make electric vehicles at least 30% of all units acquired or contracted annually. In previous years, incentives for electric buses were limited to waivers of import duties or value added taxes; this was not enough to make them competitive with diesel units.

Stay close to customers to better understand their needs and be able to significantly adapt electric bus configuration for different cities; these adaptations should consider the features of the routes, the available charging infrastructure and local climate conditions. For example, BYD, the largest Chinese manufacturer of electric buses, entered into an agreement with Egypt to create a large assembly hub for both the needs of the domestic market and export to North Africa.

Understand the requirements of both the PTA and PTO. If the customer is a PTO, it will have to fulfill PTAs’ requirements to win tenders. By understanding both stakeholders, OEMs can get competitive advantage.

Over time, change the production model from integration of electrical components into traditional bus platforms to developing new electric bus concepts from scratch that fully take advantage of electric mobility (this is what happened with electric cars).

Provide a range of different products in the electric bus portfolio. For example, the award to BYD in Bogota includes units of 80, 50 and 40 passengers. However, BYD was also prepared to offer an extra-long model of 27 meters for 250 passengers, which would better suit some of the routes in the city.

Develop technical and business solutions for battery recycling and alternative usage in advance. OEMs need to be prepared for the risk of battery failure ahead of schedule, as some operators may require replacing batteries after reducing their capacity by almost 10%. A successful example is Volvo, which is researching the use of bus batteries to store solar energy to supply residential buildings. Another example is BYD. In China, according to government regulations, OEMs should take responsibility for battery recycling. The government requests that battery manufacturers put a bar code on each battery pack to ensure traceability for the whole life cycle. BYD has developed retired-battery collection channels, which mainly rely on authorized dealers. The dealers collect and store batteries and send them to BYD’s designated factories for inspection. Reusable batteries are used for either family energy storage or telecommunications base stations. A strategic collaboration has been set up with China Tower for the second of these options. BYD is also collaborating with GEM, a major Chinese battery recycler, to withdraw precious metals such as cobalt and nickel to build new batteries.

JOBS

|  DORVAL DORVAL Full time Full time |

| STE-JULIE Full time |

| BOISBRIAND Permanent |

| LASALLE Full time |

| MIRABEL Full time |