COVID-19 Update from DAC

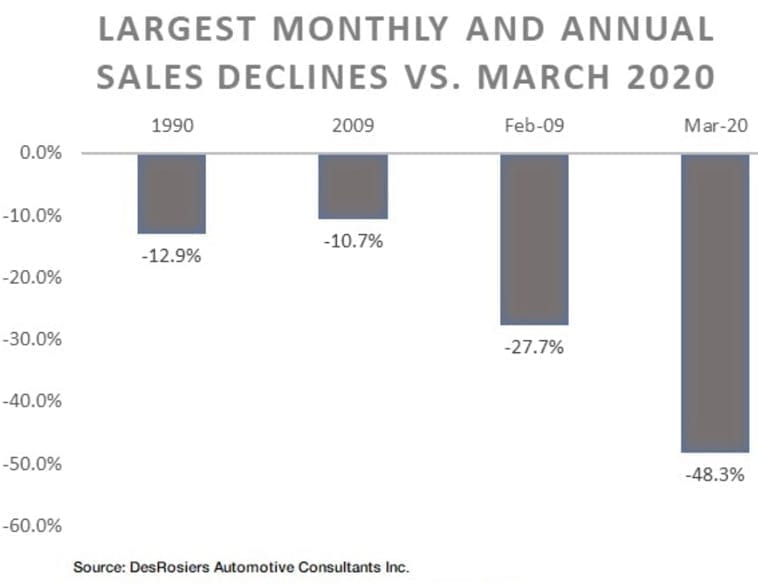

DAC has gone back through our 30 years of detailed databases and looked at the previous most severe drops seen in the new vehicle market. (Photo : DAC)

In the first client communication that Desrosiers Automotive Consultants sent out on the COVID-19 issue we mentioned three big unknowns:

- How bad is it going to be?

- How long will it last?

- What will the recovery curve look like?

At DAC, they have consistently been of the view that the answer to the first question is that the current downturn will be of an unprecedented level of severity. Indeed, the sales outlook we put out in March was significantly more negative than the numbers being forecast by others in the finance and consulting community at the time.

Having recently processed and analysed the light vehicle sales data for March, teams are holding to their view. There is no possible sugar coating the severity of the problem. The second and third questions are still obviously evolving.

To illustrate the uncharted territory in which we find ourselves DAC has gone back through our 30 years of detailed databases and looked at the previous most severe drops seen in the new vehicle market.

On a monthly basis versus the previous year the most severe decline was seen in February 2009 with a 27.7% decline versus February 2008. This drop was almost doubled by the 48.3% decline we saw in March. April will undoubtedly be significantly worse with a decline expected of a far greater magnitude.

From an annual perspective the largest annual declines in our records are during the oil price shock and subsequent recession of 1990/91 and during the financial crisis of 2008/09. The new light vehicle market in 1990 declined by 12.9% from 1989 and by 10.7% in 2009 over 2008. Again, we are anticipating a significantly more severe decline in the new light vehicle market in 2020 with our baseline scenario currently showing a decline of 25-30%.

DAC has over the past weeks completed a detailed update of our forecast for the new light vehicle market by segment and region and are sharing the detailed information with our clients. The company is still working on forecasts for the used vehicle market, the aftermarket and the vehicle finance market. As they are completed, we will continue to update you.

One factor that affects all of these areas is the usage of vehicles – kilometres driven. With millions staying at home with very little use of their vehicle, the wear and tear on vehicles will lessen significantly, and in the process lower demand across the auto sector.

When kilometres driven for the fleet as a whole decline, so does the aftermarket and vehicle scrappage, and thus ultimately used and new vehicle sales and the vehicle finance market.

At DAC we examine numerous different segmentations of the new and used vehicle markets. We have outlined just a few of them below with some of the factors we are currently trying to quantify. It should be noted that these segments we listed as examples have extensive correlation – for example luxury buyers overlap significantly with buyers coming off of a lease. We don’t pretend to have answers to all these questions but wanted to highlight some of the key areas of the market we are looking at.

— Terry Chung, Desrosiers Automotive Consultants

It is important to understand that the new and used vehicle market is not homogeneous

Selected Segments for New or Used Vehicles

Fleet buyers (executive, daily rental, commercial, etc.)

- Primarily new vehicle buyers with few used vehicle purchases

- About 18-20 percent of new light vehicle sales are to fleets so normally 350-400K each year

- One of the hardest hit groups although some small positives in delivery vehicles

- Some dealers play heavily into this market others avoid it so the impact on dealers is very mixed

- Likely limited catch up with these purchases since fleet replacement rates are very closely tied to usage.

End of lease retail customers

- They usually buy another new vehicle although there could be some leakage to the used vehicle market – becoming a used vehicle buyer through lease buy-out or other purchase

- This group could form a core group of buyers even during the worst of the economic shut down period or they would have to abandon personal use transportation – we think the numbers dropping out of the market totally will be limited

- We estimate that about 500-600K consumers are in this situation this year. A significant percentage of these consumers will still be in the market – it is more a case of whether they buy a new or used vehicle (through lease buy-out or other.

Premium/Luxury buyers

- A very high new vehicle buyer group

- About 75 percent plus lease so this group overlaps with comments about off-lease buyers

- Significantly impacted by the “wealth effect” and perceived financial outlook

- We expect the luxury/premium market to be severely hit in the short term

Needs-based buyers (new employment or vehicle replacement)

- High both new and used vehicle buyer

- This is arguably the largest of all the groups

- Significant impact on this group of the reduced kilometres driven. The group is expected to pause vehicle purchases until the economic situation normalises. They could be the most positive group influencing a return to a stronger new and used vehicle market

- One major question is whether some in this category who normally buy a new vehicle will switch to buying a used vehicle?

Buyers with a changing family situation (marriage, divorce, death, children)

- More likely new than used although many exceptions

- Largely a subset of the needs-based category but often with stronger motivation

- Likely one of the less impacted market segments in relative terms although again a pause in activity is expected

Scrapped/written off vehicle

- Primary used vehicle buyers if scrapped due to age. Primarily new if written off while their vehicle is young

- A huge group … DAC models show that 1.6 million vehicles were scrapped last year and the forecast was for this to increase

- We suspect that scrappage will go down this year. Future outlook uncertain depending on the nature of the recovery curve and rate of re-establishment of service sector jobs

For more on these issues and what they mean in specific volume forecasts for the various segments of the Canadian vehicle market contact Calvin Leung ([email protected]).

Tags : COVID-19

JOBS

|  LAVAL LAVAL Full time Full time |

| JOLIETTE Full time |

| JOLIETTE Full time |

| JOLIETTE Full time |

| VAUDREUIL-DORION Full time |